Savers to Investors: The SIP Model Driving Financial Inclusion and the Creation of a Financial Middle Class in India

Published: Jun 23, 2026

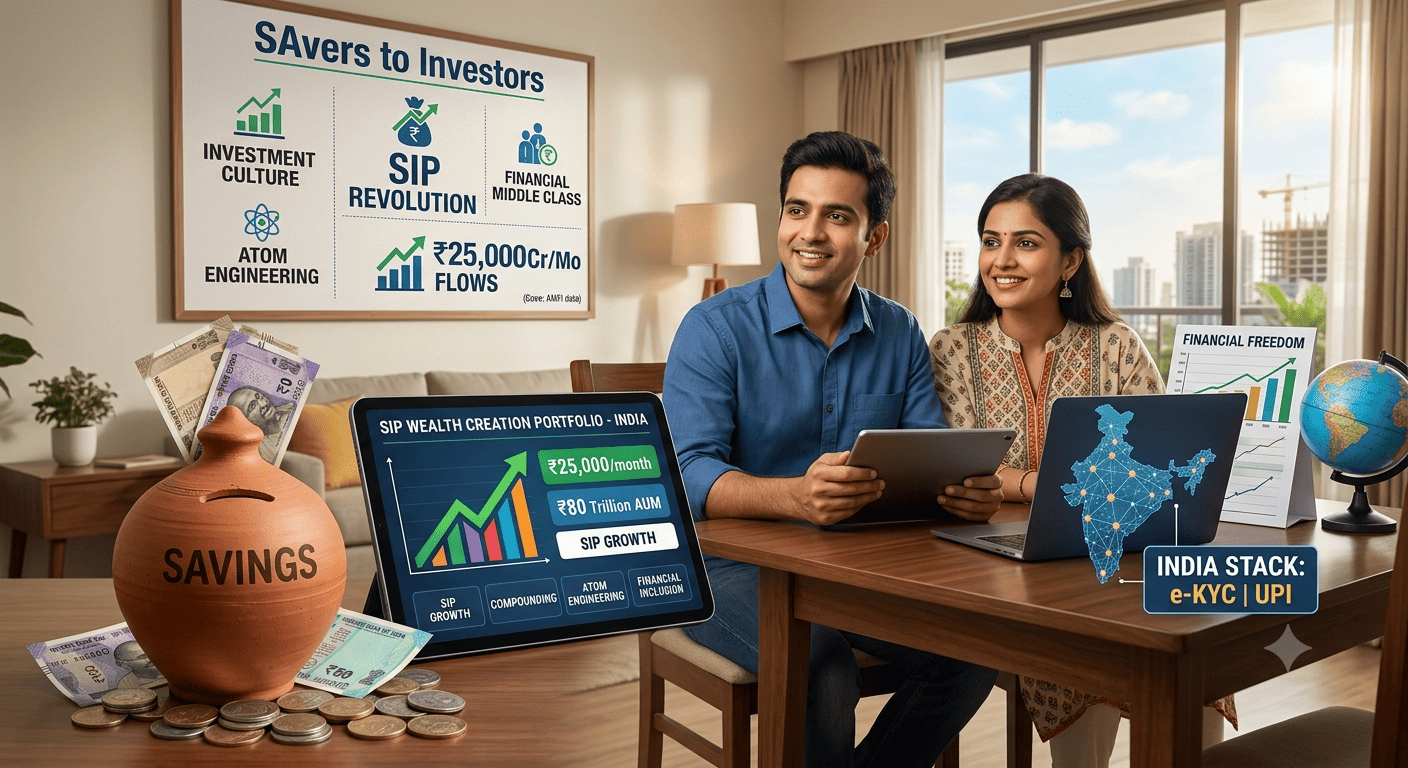

Key Points

- Financial Inclusion is reshaping India’s household savings by shifting traditional savers toward equity-linked investment vehicles like SIPs.

- Digital infrastructure such as UPI and e-KYC has reduced entry barriers, making investing more accessible and efficient for retail participants.

- Systematic Investment Plans (SIPs) promote disciplined investing through small, regular contributions that reduce market timing risks.

- The rise of SIPs has strengthened household portfolio stability through rupee cost averaging and long-term compounding benefits.

- India’s growing investment base now exceeds 100 million participants, expanding financial participation beyond urban centers.

- This shift is reinforcing a stronger, more resilient investment ecosystem driven by sustained retail participation and capital inflows.

Introduction

Digitization as the Selective Catalyst

Atom Engineering of Household Portfolios

Scale of the SIP Revolution

Pillars of Architectural Development

1. Anti-Cyclical Resilience

2. Demographically Diverse

3. Mobility Generated by Compounding Effect

The Emergence of the New Financial Middle Class

Frequently Asked Questions

1. What is Financial Inclusion in the context of investing?

Financial Inclusion refers to expanding access to formal financial systems, enabling more people to participate in investments like SIPs and mutual funds.

2. How does SIP contribute to Financial Inclusion?

SIPs support Financial Inclusion by allowing small, consistent investments, making market participation easier for first-time investors and households.

3. What role does Investment Culture play in India’s growth?

A stronger Investment Culture, supported by Financial Inclusion, encourages individuals to move from saving to long-term wealth creation through disciplined investing.

4. Why are SIPs preferred over lump-sum investing?

SIPs align with Financial Inclusion goals by reducing entry barriers and minimizing market timing risks through regular, automated contributions.

5. How has digitalization impacted investing in India?

Digital platforms have strengthened Financial Inclusion by simplifying onboarding processes and making investment access faster and more affordable.

6. What is rupee cost averaging?

It is a method where investors benefit from price fluctuations by buying more units at lower prices and fewer at higher prices over time.

7. How is Financial Inclusion improving rural investment participation?

Financial Inclusion, along with a growing Investment Culture, is enabling rural and semi-urban populations to access SIP platforms through mobile-first digital tools.

8. What risks do SIP investors reduce compared to traditional investing?

SIPs enhance Financial Inclusion by reducing emotional investing behavior and eliminating the need for market timing decisions.

9. How large is India’s retail investment base now?

India’s Financial Inclusion drive has expanded participation significantly, bringing over 100 million investors into structured market-linked systems.

10. How does long-term investing benefit wealth creation?

A mature Investment Culture supports long-term compounding, reinforcing Financial Inclusion by helping individuals build sustainable financial security.

Citations & References

[1] K. Dinesh and K. Devi, “Effectiveness of SIP based financial planning for long term wealth creation,” International Journal of Academic Excellence and Research, vol. 2, no. 2, pp. 41–48, 2026. doi: 10.62823/IJAER/02.02.203.

Available:

https://doi.org/10.62823/IJAER/02.02.203

[2] R. Nagrale and P. K. Baag, “The impact of fund size on mutual fund performance in India,” Indian Institute of Management Kozhikode Working Paper Series, no. 682, pp. 1–15, 2026.

Available:

https://www.iimk.ac.in/uploads/publications/IIMKWPS682FIN202603.pdf

[3] V. Prathibha and P. K. Pandey, “A behavioral study on investment diversification and risk perception: Evidence from salaried professionals in Bengaluru’s manufacturing industry,” International Journal of Economic Practices and Theories, vol. 15, no. 4, pp. 1276–1282, 2026. doi: 10.52783/ijept.283.

Available:

https://doi.org/10.52783/ijept.283

[4] EvePlacement. [Online].

Availabe:

https://eveplacement.com/

Streamline Your Hiring with Eve Placement

Engage, assess, and recruit top talent through tailored AI hiring challenges that go beyond resumes. Ready to hire better? Contact our research team for a custom consultation.